Central Dependency

PRESUPPOSITION

A Keynesian FUDster asks:

"Should we not take it on faith that the sudden disappearance of all central banks, all fiat money, the IMF and the BIS, would result in a multi-decade depression?"

ANALYSIS: ANCAP PERSPECTIVES

Here is a response in the Anarcho-Capitalist frame, informed by Rothbard, Mises, Bastiat, Rand, and Hoppe:

The notion is flawed: The disappearance of central banks, fiat money, the IMF, and the BIS need not lead to a multi-decade depression. To assume it would misunderstands both the nature of these institutions and the principles of a free market economy.

Economic Calculation

According to Mises' concept of economic calculation, central planning and fiat money systems distort the true valuation of goods and services. Without these distortions, market actors would have clearer price signals, leading to more rational economic behaviors rather than artificially induced booms and busts. The absence of central banks printing money would mean an end to the boom-bust cycle caused by the expansion and contraction of credit.

Natural Market Adjustments

In an Anarcho-Capitalist scenario, the market would naturally find its equilibrium. Yes, there might be short-term adjustments as markets recalibrate, but this isn't a "depression" in the classical sense. It's more akin to a reset where investments are reallocated according to real consumer demand, not artificially propped-up speculative bubbles.

Role of Gold and Commodity Money

Advocates like Rothbard argue for a return to commodity money, typically gold or silver, which inherently limits the money supply to what can be physically produced. This limitation acts as a natural check against inflation and speculative bubbles, fostering a more stable economic environment over time.

Decentralized Banking

Without central banks, banking would become decentralized, resembling more closely the free banking systems of the past. This would encourage banks to be more responsible with their lending practices, as they would not have a lender of last resort to bail them out.

Resilience and Innovation

Ayn Rand's philosophy highlights human ingenuity and rational self-interest. In such a crisis, individuals and businesses would innovate and adapt out of necessity, potentially leading to new economic structures and systems that could be more efficient and less prone to systemic failure.

Historical Precedence

Historians like Hoppe might point to historical periods before central banking where economies still flourished, albeit with different challenges. The argument here is not for a utopia but for an economy that aligns more with natural law and human action, where problems are solved through market mechanisms rather than top-down fiat.

Moral and Ethical Considerations

From an ethical standpoint, the removal of these institutions would align more with individual liberty. People would interact through voluntary exchange rather than coerced transactions enforced by government monopolies on currency.

The fear of a "depression" might stem from an attachment to the current system's familiar pains rather than an understanding of the free market's resilience and adaptability. An Anarcho-Capitalist would argue that while transition might be tumultuous, the long-term benefits of a truly free market, unencumbered by artificial monetary policies, would lead to a more sustainable, prosperous, and just economic order. The real question might be, are we willing to face the short-term pain for long-term gain in economic freedom?

REBUTTAL: What do the Keynesians say?

What are some of the strongest arguments for the continuation of the current system from notable Keynesians and prominent central bankers of today?

Stabilization of Economic Cycles

Keynesian economics posits that government intervention through fiscal and monetary policy can smooth out the business cycle. Central banks, through their control over interest rates and money supply, aim to manage inflation and unemployment, responding to economic downturns by lowering interest rates or engaging in quantitative easing, thereby preventing or mitigating recessions.

Aggregate Demand Management

According to Keynesian thought, aggregate demand (total spending in the economy) drives economic output. Central banks and fiscal policy can increase demand by stimulating spending through lower interest rates, tax cuts, or government spending, which is argued to be particularly effective during economic downturns when private investment and consumption might be insufficient.

Preventing Depressions

Advocates argue that the current system, with its Keynesian tools, has mechanisms to prevent the severe economic depressions of the past. The Great Depression, for instance, is often cited as an example of what could happen without active fiscal and monetary intervention.

Financial Stability

Central banks like the BIS and others within the G7 emphasize their role in maintaining financial stability. By acting as lenders of last resort, they prevent bank runs and systemic financial crises, providing a safety net that's considered crucial for maintaining trust in the financial system.

Global Economic Coordination

The IMF and other international financial institutions support the argument that the current system allows for better global economic coordination. This coordination can lead to policies that reduce the risk of competitive devaluations, trade wars, and other beggar-thy-neighbor policies that could exacerbate global economic instability.

Inflation Control

While not solely a Keynesian tenet, modern central banking incorporates inflation targeting, which is seen as necessary for long-term economic health. This control over inflation through monetary policy is understood to help in maintaining purchasing power and economic predictability.

Full Employment

Keynesians argue that without active policy intervention, economies might not naturally tend towards full employment. Policies aimed at stimulating demand can reduce unemployment, which not only boosts economic activity but also has social benefits, reducing poverty and social unrest.

Economic Shock Mitigation

The current system allows for quick responses to economic shocks, whether from financial crises, pandemics, or other unforeseen events. The ability to inject liquidity or enact fiscal stimulus packages is seen as indispensable for cushioning economies against sudden downturns.

Historical Success

Proponents often point to historical periods where Keynesian policies were implemented, like post-World War II economic booms, as evidence of the system's effectiveness. The argument here is that these policies led to prolonged periods of growth and stability.

Technological and Structural Change

Modern economies face rapid technological changes and structural shifts. The argument is that without a flexible monetary and fiscal policy framework, these transitions could lead to higher unemployment or economic dislocation, which the current system helps manage.

Some would argue that the current system, despite its flaws, has adapted over time. Critics within the system might advocate for reforms or tweaks rather than a complete overhaul, suggesting that while the system isn't perfect, it's capable of evolution.

For instance, discussions around negative interest rates, digital currencies, or new regulatory frameworks indicate a "willingness to adapt Keynesian tools to contemporary challenges" while maintaining the core principles of government and central bank intervention in economic management.

COUNTERPOINT: Critique of Keynesian Talking Points

An Anarcho-Capitalist or a Freedom Lover might critique each of the supposed strengths of the current centralized, debt-based, fiat monetary system as such:

Stabilization of Economic Cycles

Critique: The very act of managing economic cycles can lead to moral hazard and malinvestment. By artificially suppressing interest rates, central banks encourage risky behavior, leading to asset bubbles and subsequent busts. The boom-bust cycle isn't prevented but merely postponed or exacerbated. This intervention distorts price signals, making it harder for entrepreneurs to allocate resources efficiently.

Aggregate Demand Management

Critique: Artificially boosting demand through government spending or easy credit doesn't address underlying inefficiencies or malinvestments. Instead, it often leads to malinvestment where resources are allocated based on manipulated interest rates rather than real consumer demand. This can result in wasted capital and delayed economic correction.

Preventing Depressions

Critique: Central banks and fiscal policy might postpone or mask economic issues rather than solve them. The Great Depression's severity is often attributed to policy errors, not the lack of intervention. Anarcho-Capitalists argue that without the distortions caused by central banks, markets would naturally correct more efficiently and quickly, albeit potentially with short-term pain.

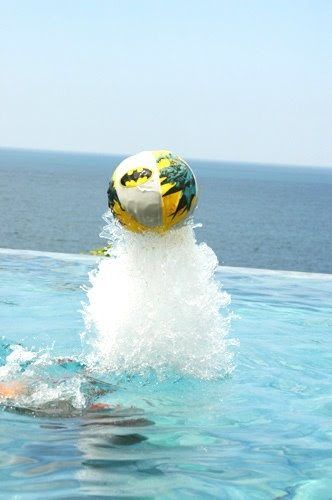

Financial Stability

Critique: Acting as a lender of last resort and bailing out failing institutions moralizes risk-taking. It creates a system where failure isn't allowed, leading to ever-larger crises due to accumulated risks. This undermines the free market's mechanism where failure is a necessary part of learning and adaptation. Like a beach ball held underwater, volatility can only be suppressed for so long.

Global Economic Coordination

Critique: Coordination often turns into coercion where nations are pressured into policies that might not align with their best interests. This can lead to a one-size-fits-all approach, ignoring unique national economic conditions. Moreover, it often serves the interests of powerful nations or institutions rather than fostering genuine free trade.

Inflation Control

Critique: Inflation targeting can lead to inflation expectations, where people anticipate and act based on future inflation, potentially leading to higher inflation rates than targeted. Moreover, central banks might prioritize inflation over other economic indicators, sometimes leading to asset inflation or employment issues.

Full Employment

Critique: Artificially low unemployment rates can be achieved by inflating the money supply, which might lead to zombie companies and individuals staying in unproductive jobs rather than moving to more innovative or efficient sectors. This creates a false sense of employment health while potentially stifling innovation and productivity.

Economic Shock Mitigation

Critique: Interventions can prolong recovery by delaying necessary market corrections. They often involve the creation of more debt, which can saddle future generations with repayment obligations or lead to currency devaluation. The focus should be on increasing resilience through free market mechanisms.

Historical Success

Critique: Historical periods of growth might be attributed to other factors like technological innovation, post-war rebuilding, or shifts in trade dynamics rather than Keynesian policies alone. Moreover, these successes often come with long-term debt accumulation or asset bubbles that eventually need addressing.

Technological and Structural Change

Critique: Government interventions can slow down adaptation by protecting old industries and delaying the shift to new technologies or economic structures. Free markets should naturally shift resources towards innovation without the lag caused by bureaucratic or monetary policy adjustments.

Anarcho-Capitalists would argue that while interventions can provide short-term relief or stability, they come at the cost of long-term economic health and individual liberty. Temporary fixes ultimately create more significant problems down the road. A system based on sound money, free banking, and minimal state intervention is the most conducive to genuine economic freedom and resilience.

CONCLUSION

Under the POSIWID theory, the Purpose Of A System Is What It Does.

We should not be surprised that those employed by the system benefit from it. Nor that they argue for its perpetual expansion.

Similarly, we should not be thrown off by claims that the results of dismantling the current system would be 'calamitous' or 'doom us to eternal depression'.

All too often, the 2nd and 3rd order consequences of a policy or institution such as Fiat Central Banking are eschewed or neglected in all but the most rigorous of philosophical explorations.

In addition to some of the negative impacts from the Fiat System mentioned above, we have things like:

- Wealth Inequality: POSIWID – The system benefits most those who receive the new money first, typically financial institutions and wealthy individuals. Whatever ends up trickling down to The Average Joe are already-depreciated-and-debased dollars.

- Savings Erosion: POSIWID – Low real interest rates remove the incentive to save and reduce capital available for investment. People are discouraged from engaging in long-term financial planning.

- Innovation Stagnation: POSIWID – Distortion of interest rates and propping up of inefficient businesses reduces the incentive for groundbreaking innovation. The quick return on speculative investments or established monopolies is more appealing than the risk of truly innovative ventures.

- Dependency on Centralized Control: POSIWID – Over-reliance on central banks for economic management reduces economic resilience and adaptability at the level of individuals and society on the whole. This makes economies more vulnerable to policy errors or external shocks.

POSIWID: The Purpose Of A System Is What It Does

If we were to design a system that would avoid these bad outcomes, what might it look like?

I think it would look a lot like the Austrians and Ancaps envisioned: One based on sound money, independent and decentralized banking, and market-driven interest rates.

Until the coming of Valhalla (Ancapistan), take what measures you can to protect your wealth and exercise your sovereignty. You may not change the world, but you can look after your own.